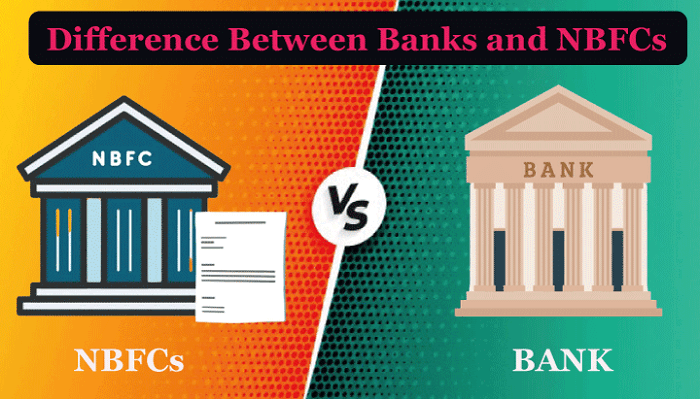

NBCFs and Banks both go about as monetary delegates and proposition genuinely comparable administrations. Be that as it may, there are many places of distinction. There are exceptionally rigid authorizing guidelines for banks when contrasted with NBFCs.

What is a NBFC?

Head business exercises of a Non-Banking Monetary Organization comprise of loaning or monetary renting or recruit buy, tolerating store or procurement of offers, stocks, bonds, and so on. To start any business they are expected to gain a permit from RBI and they are controlled by RBI.

In view of Responsibility, NBFC can be Store taking or Non-store taking. NBFC can be of following classes:

Credit Organization

Resource Money Organization

Speculation Organization

What is a Bank?

Banks perform exercises like giving credit, request stores and give withdrawals, premium installment, actually take a look at clearing and other general utility administrations to their clients.

They rule the monetary area of the nation and give a connection as a monetary mediator among borrowers and contributors.

Key Contrasts among NBFC and Bank

Since we have independently broke down the exercises embraced by both these foundations, let us examine how NBFCs and banks contrast in nature and their functionalities.

NBFC is first consolidated as an organization under the Indian Organizations Act, 1956 and afterward apply for NBFC permit from RBI, then again bank is enrolled under Financial Guideline Act, 1949.

Banks are government approved monetary delegate which are sanctioned to get stores and award credit to the general population. In any case, NBFC is an organization that gives banking administrations to more modest segments of the general public without holding a bank permit.

Banks are approved to acknowledge request stores, yet NBFCs are not approved to acknowledge stores which are repayable on request.

As NBFCs are laid out as organizations under Organizations Act, 2013 they are permitted to acknowledge up to 100 percent unfamiliar speculations. However, banks are can acknowledge unfamiliar speculations up to 74% of their aggregate sum.

Like a bank, NBFCs don’t shape a fundamental piece of installment and settlement cycle in the country.

RBI commands the upkeep of save proportions like CRR or SLR by banks. NBFC have no such commitment.

Store Protection and Credit Assurance Partnership (DICGC) give store protection office to the contributors of banks. Such office is inaccessible on account of NBFC.

NBFC isn’t engaged with credit creation like banks accomplish for their clients.

Banks offer types of assistance like overdraft office, the issue of explorers check, move of assets, and so on. Such administrations are not given by NBFC.

NBFCs are not permitted to give checks drawn on itself like banks can.