If you are considering purchasing a home, one of the first things you should do is determine your budget. Based on your credit scores, income, and down payment, getting pre-approved for home financing can determine the maximum price and loan amount you can get. A mortgage pre-approval can demonstrate to others that you are prepared and able to purchase a home, saving you time and effort during the home search.

Additional Hints for Getting a Home Loan:

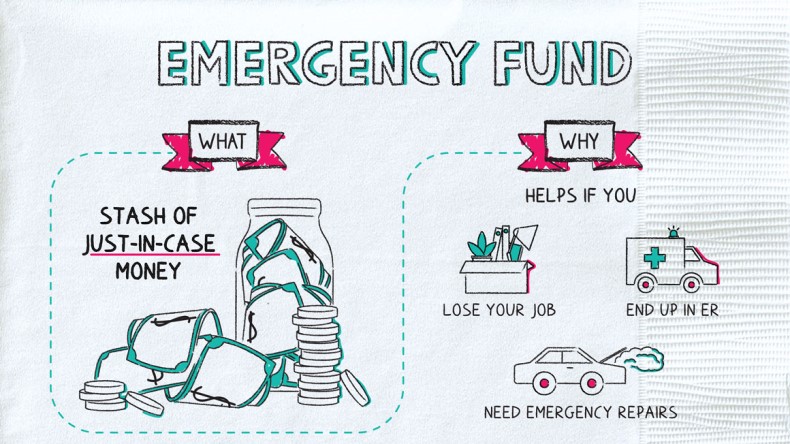

Need adaptability using a credit card issues?

An FHA mortgage permits lower credit scores than conventional home financing in addition to a low down payment. A bankruptcy discharge only lasts for two years, whereas a foreclosure discharge lasts three.

Having trouble making ends meet?

When money is tight, some lenders offer flexible mortgage terms with a 30 year fixed rate that give you the option of paying only interest or a full amortization each month.

Do you want a lower closing cost option?

You typically have the option of increasing the rate or decreasing the points if you need to cut down on your closing costs. The cost of a mortgage is set so that you can choose to pay a higher or lower interest rate.

How long do you intend to keep your mortgage?

A five-year fixed rate plan may allow you to save money on your monthly payments if you intend to keep your mortgage for less than five years. Additionally, zero-point financing might be an option.

Your debt ratio is based on how many debts you have.

A back-end debt ratio is determined by combining a mortgage’s monthly debt payments with the following: minimum payments on credit cards, loans for cars, personal loans, student loans, alimony, child support, and tax liens.

Is it necessary for you to have an impound account?

Money from the monthly loan payment is put into an impound account to pay for insurance and property taxes. It’s generally expected on contracts with under 20% up front installment.

Using an FHA mortgage to buy a condo?

For an FHA loan, a condominium project must be approved by the FHA. The FHA spot loan program is intended to provide financing for a single unit in the event that the project is rejected.

How about establishing brand-new credit accounts?

Your credit scores can drop if you apply for a new credit card or finance a purchase just before or during the mortgage process. Lower credit scores can result in a higher rate or worse.

Is it safe to say that you are arranging a task or vocation change?

Wait until after your new mortgage has been funded if you intend to make a job change, particularly if the change involves commission or a different line of work, to avoid creating a potential issue.